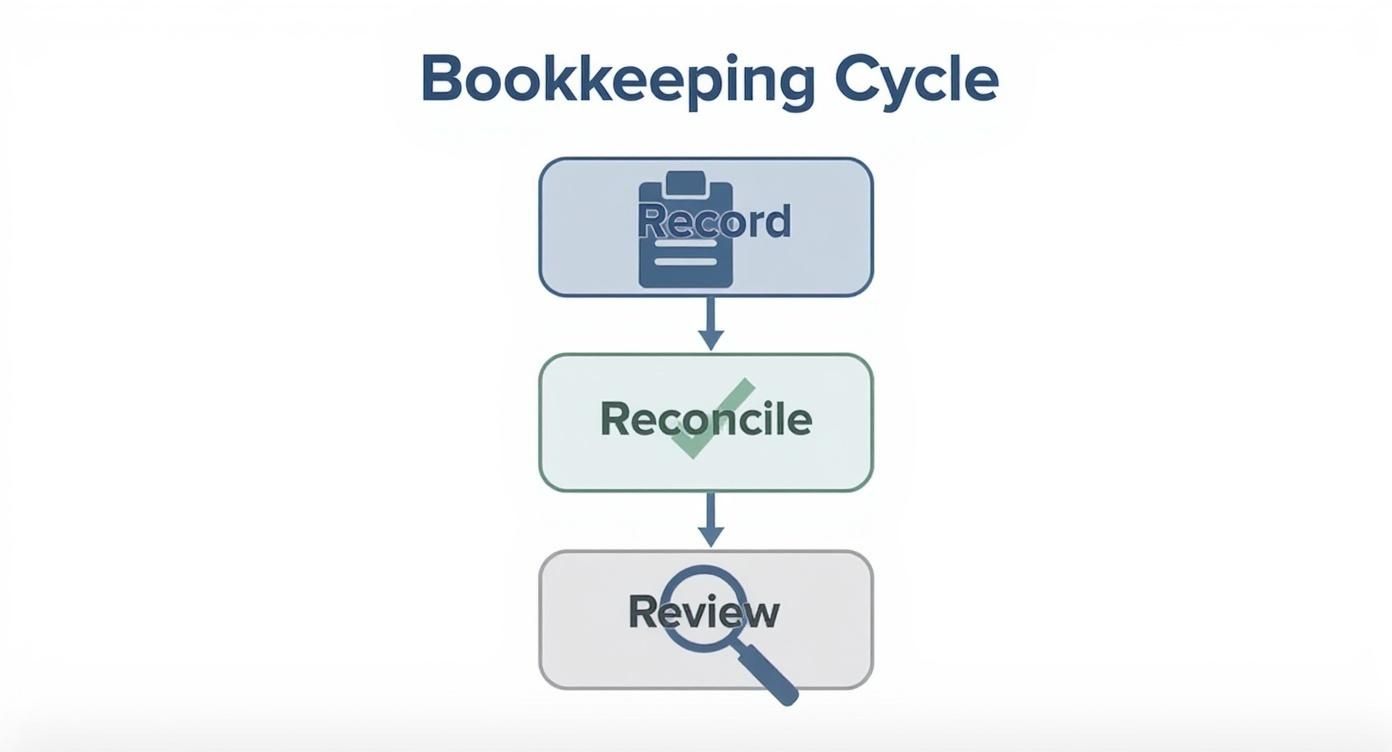

Learning how to do your own bookkeeping is more straightforward than you might think. It comes down to a simple, repeatable cycle: record your income and expenses, reconcile your accounts to ensure accuracy, and review your financial reports to understand the big picture.

Once you establish this rhythm, you can replace financial stress with clarity. Your books will stop being a chore and start being a powerful tool for making smart business decisions.

Your Path to Financial Clarity Starts Here

Are you feeling overwhelmed by receipts, invoices, and disorganized spreadsheets? If so, you’re not alone. For many small business owners, bookkeeping is a constant source of stress—something often pushed aside until tax season arrives.

But what if your books could become a source of confidence? Good bookkeeping is the engine that keeps your business healthy. It gives you the real-time information you need to solve problems before they grow and seize opportunities as they arise.

This guide will break down the entire process, from choosing the right software to understanding what your financial reports are telling you. The goal is simple: to show you that you can take control of your business finances.

Why Mastering Bookkeeping Is Essential

Most people start a business because they are passionate about their work, not because they love accounting. This often creates a knowledge gap that can lead to significant challenges.

A U.S. Bank study found that 82% of small business failures are due to poor cash flow management—a problem that almost always begins with disorganized books. Additionally, surveys show that around 60% of small business owners feel they don’t know enough about accounting, which can result in overpaying taxes or missing important deductions. You can explore more data on why financial literacy is critical for small business success.

The objective isn't to turn you into a CPA overnight. It’s about building a reliable system that gives you complete confidence in your numbers. This frees you up to focus on what you love—growing your business.

A solid bookkeeping system provides clear answers to your most important questions:

Are we profitable? Your Profit & Loss statement tells you instantly.

Can we cover payroll and bills next month? Your Cash Flow statement has the answer.

What is our company worth? The Balance Sheet gives you that snapshot.

By breaking the process into small, manageable steps, we’ll help you build a routine that ends financial chaos for good. With the right system, bookkeeping becomes a key asset for building long-term success.

Building Your Bookkeeping Foundation

Before you track a single dollar, you need a solid framework. The first step is to establish your Chart of Accounts. While it may sound technical, it's simply a categorized list of all your financial accounts. It’s the backbone of your bookkeeping system, giving every dollar a specific home, whether that's "Software Subscriptions," "Client Revenue," or "Office Supplies."

A well-organized Chart of Accounts allows you to see exactly where your money comes from and where it goes. This clarity is essential for generating accurate financial reports and making informed business decisions.

Choosing Your Accounting Software

While you could start with a spreadsheet, modern accounting software is designed to save you time, reduce errors, and grow with your business. The right tool can turn complex tasks into simple, automated workflows.

There are many options available, but for most small businesses, a few key players stand out. The best fit will depend on your business type and comfort level with technology.

A Comparison of Top Accounting Software

| Software | Best For | Key Features | Starting Price (Approx.) |

|---|---|---|---|

| QuickBooks Online | Businesses of all sizes needing robust features, reporting, and a vast ecosystem of app integrations. | – Comprehensive reporting | |

| – Invoicing and payments | |||

| – Strong mobile app | |||

| – Scalable plans | $30/month | ||

| Xero | Service-based businesses, freelancers, and those who prioritize a clean, user-friendly interface. | – Unlimited users | |

| – Simple bank reconciliation | |||

| – Project tracking | |||

| – Great for collaboration | $15/month | ||

| Wave | Solopreneurs and freelancers on a tight budget who need basic invoicing and accounting. | – Free accounting & invoicing | |

| – Receipt scanning | |||

| – Pay-per-use payment processing | Free | ||

| FreshBooks | Service-based businesses who focus heavily on invoicing, time tracking, and project management. | – Excellent time tracking | |

| – Customizable invoices | |||

| – Project profitability tools | |||

| – Retainer management | $19/month |

The goal is to choose a platform that feels intuitive to you and meets your specific needs without being overwhelming. Most offer free trials, so you can test them before committing.

The Non-Negotiable Rule: Separate Your Finances

One of the most common mistakes new business owners make is mixing personal and business finances. Using your personal checking account for a business expense or paying a personal bill from your business account creates a complicated financial tangle that is difficult to unravel, especially at tax time.

Keeping your finances separate is crucial for several key reasons:

Accuracy: It ensures your business reports accurately reflect the financial health of your company, not your personal spending habits.

Compliance: It makes tax preparation significantly simpler and protects you in the event of an audit.

Liability Protection: For LLCs and corporations, it helps maintain the legal "corporate veil" between you and your business.

From the very beginning, open a dedicated business checking account and get a business credit card. Use them for all business-related income and expenses. This simple discipline will save you significant stress and confusion.

The entire bookkeeping process can be visualized as a simple, continuous cycle.

This visual shows how each step flows logically into the next, creating a repeatable system for keeping your finances in order.

Automate Your Workflow with Bank Feeds

The adoption of cloud accounting has transformed how small businesses manage their finances. Research shows that around 64.4% of small businesses now use accounting software. Those who adopt these tools often see revenue growth of about 15%, largely due to automation features like bank feeds. You can find more insights on the impact of accounting software in recent studies.

Pro Tip: Connecting your business bank and credit card accounts to your accounting software is the single most effective step you can take. It automates data entry and helps prevent costly mistakes.

Once your bank accounts are connected, your software will automatically import new transactions each day. Your job then shifts from manual data entry to simply reviewing and categorizing these transactions using your Chart of Accounts. This turns a multi-hour task into a quick daily or weekly review. With this foundation in place, you’re ready to build consistent habits that will keep your finances clear and current.

Mastering Your Daily, Weekly, And Monthly Routines

The key to stress-free bookkeeping is consistency. Letting tasks accumulate creates a large, intimidating project. The best approach is to break everything down into manageable routines you can stick with.

This turns bookkeeping from a dreaded chore into a simple, repeatable habit. When you establish a rhythm for your financial tasks, you remain in control. You can identify small issues before they become big problems, maintain predictable cash flow, and always know exactly where your business stands.

Let's look at what this means on a daily, weekly, and monthly basis.

The Five-Minute Daily Check-In

Your daily routine should only take a few minutes, but these small actions prevent a mountain of work later. Think of it as tidying your financial workspace at the end of each day.

The goal is to capture information while it's fresh. Whether you bought supplies for a job or took a client to lunch, that receipt needs to be recorded promptly.

A couple of simple daily habits make all the difference:

Snap Your Receipts: Use your accounting software's mobile app (like QuickBooks or Wave) to photograph every physical receipt immediately after a purchase. This digitizes the record and prepares it for categorization.

Categorize New Transactions: Log in to your software and check your bank feed. Since it imports transactions automatically, you’ll see new items from the past 24 hours. Quickly categorize them—assigning a gas station charge to "Vehicle Expenses" or a client payment to "Service Income."

This simple process ensures your books are always close to real-time, giving you an accurate view of your cash position.

Your Weekly Financial Rhythm

Once a week, set aside 30-60 minutes to handle tasks that keep your business running smoothly. This is when you actively manage your cash flow, ensuring money is moving as expected.

This weekly touchpoint is crucial for maintaining healthy relationships with your customers and vendors. It prevents late payments, keeps your team paid, and provides a clear view of your short-term financial obligations.

Your weekly checklist should include:

Process Payroll: If you have employees, running payroll on time is a top priority. Ensure all hours are approved and run the payroll cycle so your team is paid correctly and on schedule.

Pay Your Bills: Review any outstanding bills from suppliers or contractors. Schedule payments for those that are due to avoid late fees and maintain good vendor relationships.

Send and Follow Up on Invoices: Send invoices for any completed work. Just as importantly, check your accounts receivable and send a polite reminder for any past-due invoices.

A consistent weekly routine is the engine of healthy cash flow. By staying on top of invoices and bills, you're not just doing bookkeeping; you're actively managing the lifeblood of your business.

The Essential Monthly Review

Your monthly routine is the most comprehensive. This is when you step back to verify accuracy and look at the bigger picture. Block out two to four hours at the end of each month to perform a thorough review and close out the period.

This is your chance to confirm that the data you’ve entered all month is 100% correct. The cornerstone of this process is reconciling your accounts.

Reconciling Your Accounts

Reconciliation is the process of matching the transactions in your accounting software to your official bank and credit card statements. It’s a critical step that confirms every dollar is accounted for and that your books are an exact mirror of your bank records.

This process helps you:

Catch any bank errors or fraudulent charges immediately.

Identify any missing transactions you forgot to record.

Confirm that your financial reports are built on solid, accurate data.

After reconciling, you can confidently run your key financial statements, like the Profit & Loss and Balance Sheet. These reports will tell you the true story of your business's performance over the last month.

For a deeper look, our guide to effective monthly bookkeeping for small businesses offers more strategies to ensure your finances are always in perfect order. By establishing these simple routines, you’ll turn financial chaos into predictable clarity.

How to Read Your Financial Reports

The purpose of recording transactions and reconciling accounts is to turn that raw data into useful information. Your financial reports tell the story of your business's health.

Think of them not as dense accounting documents, but as a report card showing what’s working, what isn’t, and where your business is headed. You don't need a finance degree to understand them. By focusing on three core reports, you can get a clear picture of your performance.

Let's break them down in simple, practical terms.

The Profit and Loss Statement: Your Profitability Scorecard

Often called the P&L or Income Statement, this report answers the most critical business question: Are we making money? It totals your revenue and subtracts all your expenses over a specific period—like a month, quarter, or year—to show your net profit or loss.

Here’s a quick summary of what you'll see:

Revenue (or Income): The top line, showing all the money earned from sales.

Cost of Goods Sold (COGS): The direct costs of producing your product or delivering your service. For a carpenter, this would be lumber and nails.

Gross Profit: Your revenue minus COGS. This is what’s left to pay for all other business expenses.

Operating Expenses: The costs to run the business, such as rent, marketing, software subscriptions, and administrative payroll.

Net Income (Profit): The "bottom line." After every expense is subtracted from your revenue, this is what remains. If it’s negative, it’s a net loss.

Reviewing your P&L regularly helps you spot trends. Are your software costs increasing? Is your revenue growing faster than your marketing spend? This report provides the answers.

The Balance Sheet: A Snapshot of Your Net Worth

While the P&L measures performance over time, the Balance Sheet provides a snapshot of your company's financial position on a single day. It answers the question: What is my business worth?

It is based on one simple formula: Assets = Liabilities + Equity.

Assets: Everything your business owns that has value, such as cash, unpaid customer invoices (accounts receivable), inventory, and equipment.

Liabilities: Everything your business owes, including credit card debt, loans, and supplier bills (accounts payable).

Equity: What remains for the owner after all liabilities are paid. It represents your stake in the company.

A healthy balance sheet is a powerful indicator of financial stability. It demonstrates to lenders and investors that you have sufficient assets to cover your debts, giving them confidence in your business.

The Statement of Cash Flows: Where Your Money Actually Goes

Have you ever looked at a profitable P&L statement while your bank account is nearly empty? The Statement of Cash Flows explains this common scenario. It tracks the actual cash moving in and out of your business, broken down into three areas.

Operating Activities: Cash from your core business operations—customer payments and payments to suppliers and employees.

Investing Activities: Cash used to buy or sell long-term assets, like a new vehicle or equipment.

Financing Activities: Cash from investors or lenders (like a loan) and cash paid to owners (draws).

This report is vital for managing your day-to-day finances. It helps you determine if you will have enough cash to make payroll or pay rent next month, making it your best tool for avoiding a cash crunch.

Understanding these reports moves you from just "doing the books" to using your financial data to make smart, strategic decisions.

For those who want to see these numbers in real-time, building a financial dashboard for your small business provides an at-a-glance view of these key metrics.

Knowing When to Get Professional Help

Doing your own bookkeeping is an valuable skill. It puts you in control of your business's financial health. But as your company grows, the time spent categorizing expenses and reconciling accounts is time taken away from your customers, your team, and your long-term strategy.

At a certain point, the DIY approach may stop being an effective use of your energy. Recognizing this moment is not a sign of failure—it's a strategic business decision. It’s about investing in expertise so you can get back to doing what you do best.

Key Signs It's Time to Outsource

How do you know when you’ve reached that turning point? The signs are usually clear. If any of the following sound familiar, it may be time to seek professional help.

You're spending too much time on bookkeeping. If your books are taking up more than a few hours a week, that is valuable time that could be redirected to revenue-generating activities.

Your books are falling behind. If you are months behind on reconciling your accounts, you have a dangerous blind spot, making it impossible to accurately gauge your cash flow or profitability. For many business owners in this position, a professional bookkeeping cleanup service is the first step toward regaining clarity.

You're not confident about compliance. Payroll taxes, sales tax filings, and year-end reporting have strict rules and deadlines. Uncertainty in these areas can lead to costly penalties and unnecessary stress.

Your business is becoming more complex. Hiring your first employee, taking on a large loan, or expanding to a new state all add layers of financial complexity. A professional can manage this without missing important details.

Outsourcing isn’t an expense; it's an investment in accuracy, compliance, and your own time. It frees you up to be the leader your business needs.

What Kind of Help Do You Need?

Bringing in a professional doesn’t have to be an all-or-nothing decision. You can find support that matches your specific needs and budget.

Monthly Bookkeeping Services: This is a popular choice. A firm handles all your monthly tasks—categorizing transactions, reconciling accounts, and preparing your core financial reports.

Payroll Management: If managing payroll, withholdings, and tax filings feels overwhelming, you can outsource just that component. It ensures your team is paid correctly and on time.

CFO and Advisory Services: For businesses focused on significant growth, a fractional CFO can assist with budgeting, forecasting, and profitability analysis, turning your financial data into a strategic roadmap.

This shift toward outsourcing is becoming more common. Around 78% of small businesses now prefer to outsource their bookkeeping tasks. Business owners are realizing that the time savings and increased accuracy from a specialist far outweigh the costs. You can learn more about how bookkeeping professionals drive business success and why so many are making the change.

Still Have Questions? Let's Clear a Few Things Up.

Even with a solid plan, questions will come up as you manage your business finances. That's completely normal. Here are answers to some of the most common questions we hear from business owners.

What’s the Real Difference Between Bookkeeping and Accounting?

Think of it this way: bookkeeping is the process of recording and organizing financial data, while accounting is the process of interpreting that data to make informed decisions.

A bookkeeper handles the essential, day-to-day work of recording every transaction and categorizing it correctly. This detailed process ensures your records are clean and accurate.

An accountant takes a higher-level view. They analyze, interpret, and summarize the data organized by the bookkeeper. They prepare tax returns, help you build a financial strategy, and turn raw numbers into a clear story about your business's health. In short, a bookkeeper creates the records; an accountant helps you make sense of them.

Can't I Just Get By with a Spreadsheet for Now?

It can be tempting to use a spreadsheet, especially when you're just starting and trying to save money. However, relying on spreadsheets is a risk that you will likely outgrow quickly.

Spreadsheets are prone to human error. A single broken formula or an accidentally deleted row can disrupt your entire year's financials. They also lack automation, meaning you have to manually enter every transaction from your bank statements, which is a significant time commitment.

Modern accounting software like QuickBooks or Xero is designed to prevent these problems. It imports your bank data automatically, reduces costly mistakes, and generates professional reports with just a few clicks. You'll be glad you made the switch, especially at tax time.

How Often Do I Really Need to Reconcile My Bank Accounts?

This is non-negotiable: you must reconcile every business bank and credit card account at least once a month.

Reconciliation is the process of matching the transactions in your accounting software with your official bank statement, line by line. It confirms that your books are a perfect mirror of what the bank reports.

This monthly check-in is your first line of defense to:

Catch bank errors or fraudulent charges right away.

Identify any transactions you forgot to record.

Guarantee that the financial reports you use for decision-making are based on 100% accurate data.

Performing this task consistently gives you—and your accountant—complete confidence that your numbers are correct.

Feeling confident about your finances shouldn't be a luxury. If you're ready to trade bookkeeping stress for complete clarity, the team at Accuracy Accounting & Consulting is here to help. We turn messy books into decision-ready financials so you can focus on growth.

Schedule a consultation with our team today to get your books in order and keep them that way.